09 Jul 2024 COMMERCIAL STAMP DUTY CHANGES NOW IN EFFECT

What you need to know about Victoria’s Commercial Property Tax reform

On 1 July 2024, the Victorian Government’s new Commercial and Industrial Property Tax (CIPT) came into effect.

It’s been created to replace land transfer duty (stamp duty) in an attempt to support business investment, encourage businesses to expand or relocate, and promote more efficient use of commercial and industrial land.

Perhaps the most interesting aspect is that, because the transition to the new tax takes 10 years, there is an option for the final stamp duty payment to be spread over 10 annual payments rather than being paid in full at settlement (details below).

How CIPT will be applied

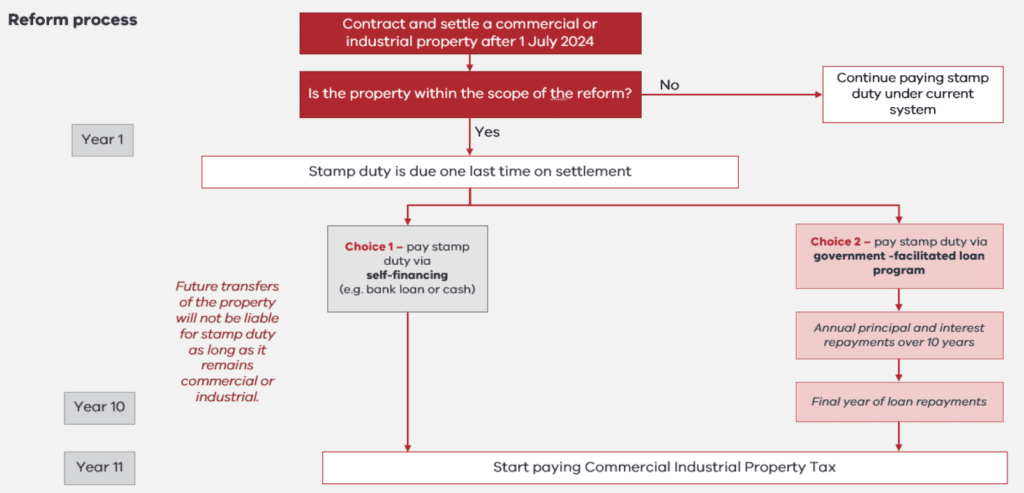

From now on, the first time a contract of sale is entered into for an eligible property (both the signing and completion of the contract of sale being after 1 July 2024), it will become part of the new CIPT system. This is called the ‘entry transaction’.

The entry transaction will still be subject to stamp duty, however, this will be the final time stamp duty will be paid on that property as it begins a 10-year transition period to CIPT.

The new Commercial and Industrial Property Tax will then be payable for the first time 10 years after the final stamp duty payment, regardless of whether that property has transacted again.

CIPT will be set at a flat one per cent of the property’s unimproved land value (or ‘site value’). A concessional rate of 0.5% will apply to ‘BTR land’ (land that qualifies for a build-to-rent land tax benefit).

It is a replacement for stamp duty and separate to land tax, which will continue to apply.

As an annual tax, CIPT is likely to be deductible for income tax purposes just as land tax is.

How a property enters the CIPT system

Entry into the new system will occur when:

- A contract for sale is entered into on or after 1 July 2024 (i.e. both signing and completion need to occur on or after 1 July 2024);

- There is a 50% or more change in ownership of the property – via either a dealing in the property itself or indirectly via a dealing in shares or units; and

- There is a relevant “positive duty liability” – that is, duty needs to be paid under an eligible type of transaction (including where certain concessions apply, such as the 50% regional commercial and industrial concession). This can include either transfer duty or landholder duty.

The property will not enter into the new system if:

- The transaction is exempt from duty – e.g. under an exemption for deceased estates, charitable institutions, or transfers between spouses.

- The duty is triggered under an excluded / complex arrangement – e.g. corporate reconstruction concessions, dutiable leases, economic entitlement provisions or subsale provisions.

The final stamp duty payment can be made in annual payments

To smooth the transition to the new system, the Government will give purchasers of commercial or industrial property (who meet certain eligibility criteria) the option of accessing a government-facilitated transition loan as an alternative to self-financing the upfront stamp duty amount.

In this way, eligible purchasers can transition to an annual repayment from the time of purchase and free up capital to invest in expanding their business.

If a purchaser opts to take up the transition loan option, they’ll make annual loan repayments over 10 years equivalent to the property’s final upfront stamp duty liability plus interest.

If the property is subsequently sold or the property changes to a non-qualifying use the borrower will be obliged to repay the outstanding balance on the loan. The loan cannot be novated or transferred to a subsequent purchaser.

Some further details about the implementation of CIPT

CIPT will be based on land ownership as at 31 December following the 10th anniversary of the first transaction of the property after 1 July 2024.

Administrative arrangements for CIPT will largely align with those already in place for land tax. Similar to land tax, you will be able to pay CIPT in a single annual payment or by instalments.

If you’re planning a commercial property transaction and want clarity on the tax and structural implications, our business advisory services can help you navigate the new CIPT rules with confidence.

Consistent with land tax, CIPT will not be allowed to be passed through by landowners to specific retail tenants identified in the Retail Leases Act 2003.

Get in touch today!

Melbourne Office

(03) 8888 4000

info@thepractice.com.au

To book your free Discovery Session with our team at The Practice, complete the form and we’ll get in contact with you.

Book your free discovery session

Leave your details below.